What is a treasury bill?

A Treasury bill (or T-Bill) is a short-term government debt security, which yields no interest. Rather, it is issued at a discount on the redemption price.

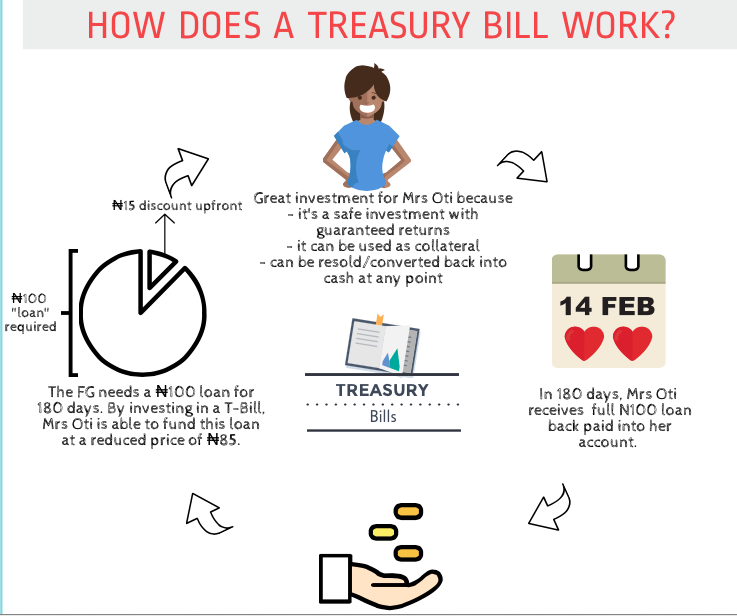

Basically, the Federal Government issues treasury bills at discounted prices for maturity periods between 91 and 364 days. At the end the selected maturity period, the government buys the bills back at full price. For example, let’s say you buy a 182-day ₦200,000 treasury bill at a discounted rate of ₦180,000. The Federal Government of Nigeria writes an IOU for ₦200,000 and agrees to pay back in 182 days. You don’t get any monthly interest payments, rather you make your money back when the bond is purchased back from you at full price. In this case the T-Bill pays 11% interest rate (₦20,000/₦180,000 = 11%) over the 182-day period.

You will not get any e-mail alerts of notifications until the end of your tenure, so don’t expect any – just be patient. You only get a debit notification when the money is taken out of your account, and a credit notification when the money is returned at the end of the tenure. If you want proof of your investment, it is best to request this from your bank once the money has left your account. You will need to ask them for a T-bill certificate after payment has been made.

Where can I purchase T-Bills?

T-Bills are sold via commercial banks and official agents such as merchant banks, and sales are open to individuals and corporate investors.

Is there a minimum purchase amount for T-Bills?

It depends on the bank. Some banks offer a minimum of ₦50,000, while some offer a minimum of ₦500,000.

How long can I invest for?

There are 3 tenures available: 91 days, 182 days or 364 days.

How can I buy T-Bills?

First, you will need to complete an application form issued by your bank or an approved discount house such as Kakawa Discount House Ltd. You will need to submit your application early, as most banks are required to submit applications received by the Wednesday before the dates announced by CBN – which you can get on the CBN website or in the dailies. Alternatively, your bank might be able to provide you with notifications ahead of time.

When completing the application form, you will be requested for a discount rate – which is the percentage by which the face value of the bill is discounted by. Current rates in Nigeria are around the 12% – 14% mark. You can request for this rate to either be set by your bank, or specified by you (under the “stop rate” section of the application form). If you do however choose to specify a rate which is significantly higher than what the CBN is prepared to offer, your bid will fail.

Various banks will offer you various stop rates/discount rates, depending on how much you want to invest and how long you want to invest it for so it is a good idea to shop around and not go with the first offer you receive. Do your research and select a bank carefully as people have reported banks offering as low as a 2.4% discount rate. As at October 2015, unverified informal accounts suggest that Firstbank seems to have the best bid rate for a 91 day tenure at 9.5%.

How do I calculate the return on my investment on T-Bills?

It is very easy to calculate the returns on your investment, and how this is paid. If for example you purchase T-Bills worth ₦100,000 at a 10% discount rate, CBN only debits your account of ₦90,000. At the end of the maturity period, you are paid your face value sum of ₦100,000.

Can I sell my T-bills before it matures?

It is possible to sell your T-Bills before it maturity using the OTC market. Because this is governed by the forces of demand and supply, you might make a loss if you choose to sell them before their maturity date.

How secure are T-Bills?

As T-Bills are based full faith of the Federal Government of Nigeria, they are considered one of the most secure investments to make. They can also be used as collateral, and are accepted by all banks.